Persistent central bank buying

Gold Outlook for 2026: Strategic Positioning and Market Dynamics

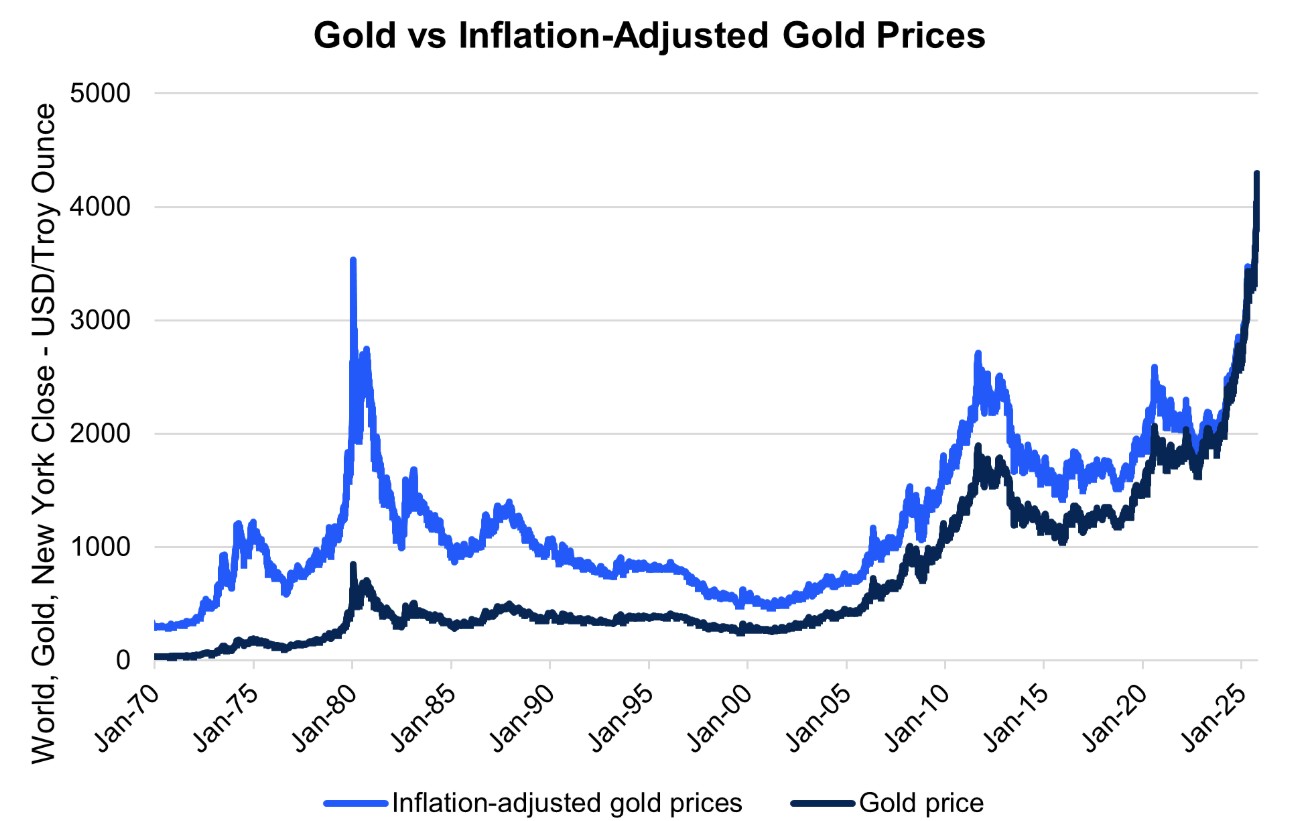

2025: An Exceptional Year for Gold

Gold delivered one of the most remarkable performances across global financial markets in 2025. Prices repeatedly established new historical records exceeding fifty times throughout the year with peak gains reaching 67%. This exceptional performance marked gold’s strongest annual gain since 1979, significantly outpacing major equity benchmarks including the S&P 500 and Nasdaq.

What distinguished 2025 was the breakdown of traditional market correlations. Historically, gold moves inversely to interest rates and risk assets. However, throughout 2025, gold and U.S. equities rose simultaneously—an unusual development signaling a fundamental shift in market pricing dynamics. This convergence reveals deeper structural changes in how investors perceive gold.

Any Platforms, Any Formats.

The People’s Bank of China demonstrated particularly notable commitment, adding gold for thirteen consecutive months. This aggressive accumulation lifted China’s gold share in foreign exchange reserves to unprecedented levels reflecting strategic reserve diversification priorities.

Beyond immediate demand dynamics, central bank buying reflects structural monetary system shifts. Growing concerns regarding U.S. fiscal sustainability and dollar credibility erosion have accelerated global reserve diversification. Gold—sanction-proof and strategically neutral—has emerged as the preferred anchor asset for central banks globally. This demand remains cycle-insensitive and price-insensitive, effectively establishing gold’s long-term valuation floor at elevated levels.

Central Bank Buying: The Structural Foundation

Central bank purchases formed the backbone of gold’s resilience at elevated levels. Global central banks maintained net buyer status for multiple consecutive years demonstrating persistent strategic demand. The first three quarters of 2025 alone witnessed net purchases reaching 634 tonnes with full-year demand expected to exceed 1,200 tonnes cumulatively.

Supporting Market Forces in 2025

Lower interest rate expectations and weakening U.S. dollar dynamics reduced the opportunity cost of holding non-yielding gold assets. Throughout 2025, markets increasingly priced Federal Reserve rate cuts pushing yields lower while simultaneously weakening the dollar—both supportive factors for gold denominated in USD. Improved global liquidity conditions associated with monetary easing cycles added substantial tailwinds.

Geopolitical and macroeconomic uncertainty played a critical supporting role throughout 2025. Persistent tensions across Ukraine, the Middle East, and Southeast Asia continued disrupting financial systems, trade routes, and supply chains. Global growth slowdown combined with recurring U.S. recession concerns created risk-sensitive market conditions. Policy uncertainty ranging from volatile tariff rhetoric to perceived threats to Federal Reserve independence made markets increasingly sensitive to systemic risk.

Gold ETF inflows totaled approximately USD 77 billion throughout 2025, highlighting sentiment and structural demand shifts. Asia—particularly China and India—experienced surging retail and institutional demand for both physical gold and ETF products. Rising prices attracted incremental capital creating a self-reinforcing upward momentum loop.

Any Platforms, Any Formats.

Three Potential 2026 Scenarios

Base Case: If global growth slows modestly while the Federal Reserve continues its easing cycle, real rates likely drift lower while the dollar weakens further. This environment reduces gold’s opportunity cost and supports continued gains, positioning gold as a defensive growth asset delivering steady positive returns rather than explosive rallies.

Bull Case: If the global economy encounters a vicious cycle with intensifying recession signals, escalating trade tensions, and surging geopolitical risks, tail risks could materialize simultaneously. Safe-haven demand may trigger sharp short-term gold price spikes. Markets could actively speculate on coordinated Federal Reserve and Trump-led rescue measures with simultaneous fiscal and monetary easing further amplifying gold’s upside.

Bear Case: If U.S. economic resilience surprises positively, the exceptionalism narrative returns to dominance, and fiscal stimulus accelerates ahead of midterm elections, re-inflation signs could emerge. The Federal Reserve might maintain higher rates longer than currently expected. Gold could face corrective pressure resembling valuation adjustments rather than structural breakdown. Equity market volatility could also force deleveraging and asset liquidation pressuring even safe-haven assets.

Can Gold Maintain Strength in 2026?

Gold retains meaningful upside potential for 2026, though repeating 2025’s extreme gains appears unlikely. The trajectory depends significantly on whether the U.S. economy slips into recession or whether the U.S. exceptionalism narrative regains traction. Short-term trading rhythms will likely be shaped by data releases and event risk, while broader trends remain anchored by structural factors.

Trading Gold in 2026: Strategic Approach

Gold remains supported by multiple structural tailwinds including persistent central bank buying, favorable dollar and rate environments, and elevated geopolitical and macroeconomic uncertainty. The path of least resistance points higher strategically.

Traders should recognize gold’s evolving portfolio role and adapt positioning flexibly. During mild slowdowns, buying on dips remains a core strategy. If extreme risk-off shocks emerge, selectively adding exposure captures short-term upside. Conversely, if growth surprises positively or the dollar strengthens materially, reducing exposure becomes essential for managing downside risk effectively.

Short-term XAUUSD volatility, cross-currency opportunities from global policy divergence, and ETF flow shifts offer valuable trading signals. Gold supply chain opportunities merit attention—rising gold prices improve mining profitability creating additional trading angles across related industries and value chains.